The imperative of boosting risk management in Emerging Asia

Chief Risk Officer

In his latest book “Thank you for being late” the New York Times columnist Thomas Friedman describes the dynamics of the interconnected and compounding forces of the Fourth Industrial Revolution, globalisation and climate change, leaving us with little “choice but to adapt to the new pace of change”.

Because this is hard and not everybody is sufficiently prepared for constant learning a sense of malaise has gripped Western societies and politics leading to some extraordinary and surprising political choices in recent months.

The phenomenon of rapid change is not confined to the Western world. Everybody working in Hong Kong can testify to the breath-taking transformation of the region.

On the positive side we witness the emergence of a new middle class society in China, India and the ASEAN countries. Millions of people are being lifted out of poverty and offered a life which is free from hunger and many of the ailments associated with poverty.

However, this doesn’t come for free: Growing pollution, rising sea levels and warming are now unpleasant facts even in seemingly remote regions such as Myanmar or the Himalayans with their melting glaciers.

Why is this relevant for an insurer? The answer is simple: These trends go to the heart of what we offer and how we do business. The core value proposition of an insurance company is to provide policyholders with peace of mind based on certainty. Against a predictable current expense, the premium payment, insurers mitigate the financial impact of uncertain future events such as accidents, typhoons and illness. In order to be able to offer this safety net the insurer needs to have a strong capital base and stable revenues. These prerequisites to meeting our customers’ expectations are being challenged by the current pace of change. How can we as an industry respond?

First and foremost, we need to further boost our risk management capabilities.

These have always been at the core of what an insurer does and have seen an evolution from mere underwriting analytics to strategic capital management.

Regulatory regimes progress from simple governance and consumer protection regimes to modern risk-based capital, management and disclosure frameworks primarily modelled on the European Union’s Solvency II regime.

Greater computing power allows for more sophisticated Economic Capital modelling. Technological progress in connectivity and dealing with complexities enables much improved risk analytics and new products which are tailored to the risk profile of the insured.

At the same time, interconnected financial markets spread systemic risks around the globe and climate change throws into doubt the relevance of historical data for underwriting purposes.

Emerging Asia adds its own set of complex challenges which need to be carefully understood when making policy decisions.

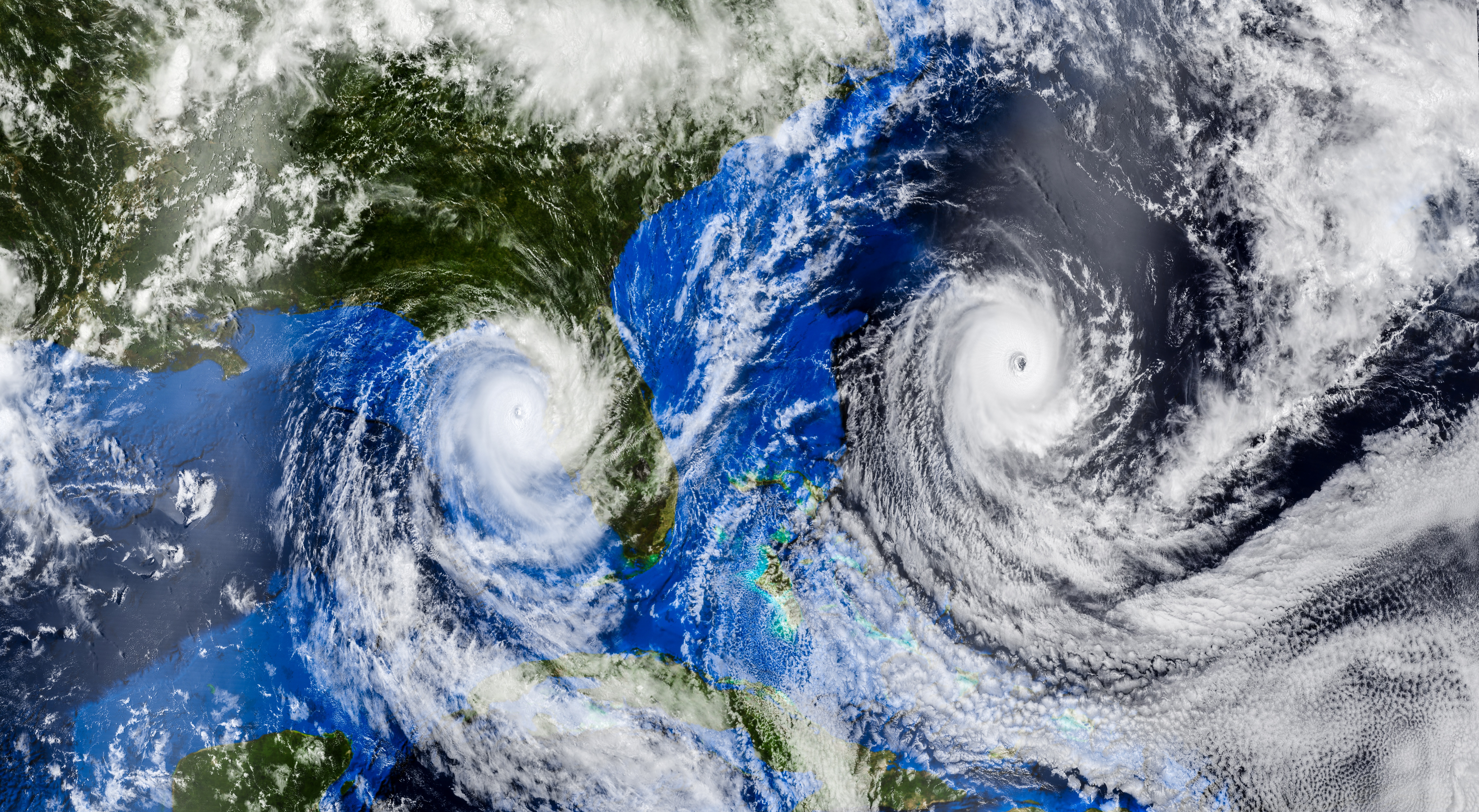

For example, even though Asia does not exhibit the highest degree of urbanisation in the world the region records the fastest rate of urban population growth. Most cities are struggling to cope with the unabated influx of people. The biggest agglomerations with 20 million and more inhabitants such as Jakarta, Manila, Mumbai and Shanghai are all exposed to rising sea levels and weather related perils whereas risk management measures such as flood protection schemes are difficult to implement.

For insurers, it becomes increasingly challenging to cover those perils as the nature of the risk constantly changes and historical data loses in value. A more forward looking approach such as scenario analysis may be a good approach to responding to these challenges.

Another example of today’s VUCA (volatile, uncertain, complex and ambiguous) world is the enormous volatility displayed by the Shanghai stock market in 2016, exceeding by far what we experienced during the 2008 global financial crisis. Other stock markets in the region went through similar situations, not least because of a lack in depth and liquidity.

These challenges are exacerbated by the fact that emerging Asia’s bond markets are still immature and underdeveloped, therefore not qualifying as an alternative to stock markets: While Asia’s share in global emerging market GDP of about 70% is matched by its share in emerging market equities, the region’s share in bond markets is less than 30%.

Insurers with long-term liabilities find it difficult to match durations. This regional peculiarity has to be taken into account when building a risk-based capital approach to investment risk and Asian regulators should resist the temptation of just replicating Europe’s preference for fixed-income instruments into RBC models. Instead, long-term investments in infrastructure or real estate should be carefully considered as they address both the needs of many economies in Asia and insurers’ asset-liability management constraints.

In order to effectively deal with the risks in an era of accelerating change and to address the specific challenges facing emerging Asia regulators and risk managers need to strike the right balance between quantitative and qualitative approaches.

This is precisely the philosophy underlying Solvency II (though sometimes hidden under complexities) and its three pillars of capital requirements, risk management and risk disclosure.

For Boards and management teams, the benefits from adopting this mind-set go far beyond regulatory compliance. It is also set to help insurers do the right things and do these right.

Other Insights

Wed, 22 Apr 2026

| 16 mins

|

Frankie Chan

Tue, 24 Mar 2026

| 19 mins

|

Kritika Kashyap

Fri, 30 Jan 2026

| 18 mins

|

Kritika Kashyap

Mon, 27 Oct 2025

| 10 mins

|

Kritika Kashyap

Elevate Your Business

with Peak Re

with Peak Re